Imagine a cryptocurrency exchange fully licensed and operating legally within the European Union in early April 2026. While everything seems fine now, the team is keenly aware of a crucial deadline on July 1st. The founder is confident they have enough time – about 90 days – to finalize all necessary licensing requirements and remain compliant.

MiCA Decoded is a 12-article weekly series for Bitcoin.com News, co-authored by LegalBison’s Co-Founding and Managing Directors: Aaron Glauberman, Viktor Juskin and Sabir Alijev. LegalBison advises crypto and FinTech companies on MiCA licensing, CASP and VASP applications, and regulatory structuring across Europe and beyond.

That idea has a weakness. Depending on where you are, that weakness might be impossible to fix.

Myth 1: The Deadline Most Service Providers Got Wrong

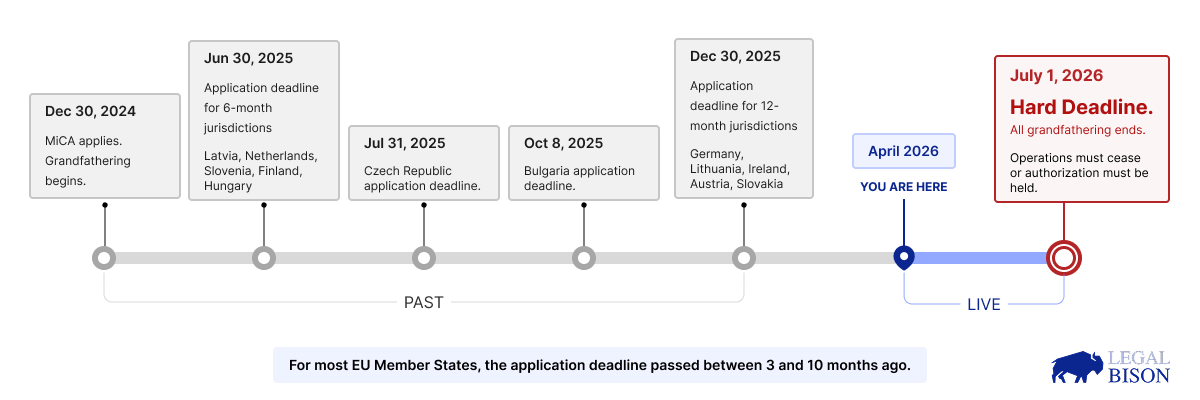

Crypto companies must be officially authorized by July 1, 2026, or they will have to stop operating. The rest of this article explains what happens depending on whether they meet that requirement.

Article 143(3) of MiCA states that service providers operating lawfully before December 30, 2024, may continue to do so until July 1, 2026, or until they are granted or refused authorization, whichever comes first.

The word is “granted.” Not “applied for.” Not “in progress.”

Getting approved can take several months, depending on where you apply and how complete your application is. If a service provider hasn’t submitted their application by April 2026, they won’t have enough time to meet licensing requirements.

In nearly all EU countries, the period where existing systems were automatically allowed to continue is over. Now, the focus has shifted to determining if businesses can still operate legally, and what steps are needed to ensure they can.

Myth 1: “I Was Registered Before December 2024, So I’m Covered Until July”

Becoming automatically approved under MiCA isn’t guaranteed for existing registered VASPs. Approval was always dependent on meeting certain requirements, and a key one was a deadline set by each individual EU country. To qualify for temporary protection, service providers had to formally apply for authorization *before* that country’s specific deadline.

Those deadlines, for the majority of EU Member States, are gone.

According to ESMA’s published list of grandfathering periods, the Czech Republic set its deadline at July 31, 2025. Bulgaria closed its window on October 8, 2025. Germany, Lithuania, Ireland, Austria, and Slovakia all had 12-month periods from December 30, 2024, placing their deadlines around the end of December 2025. The majority of EU Member States set application deadlines that are now several months in the past.

If a VASP was registered before December 30, 2024, but didn’t submit a complete application by the deadline set by its country, it won’t be protected under grandfathering rules in that country. This means the strict July 1st deadline will apply immediately, without the flexibility the temporary rules were meant to offer.

A related question surfaces immediately: could a VASP registration in one Member State be used to passport services into another during the transitional period?

The answer is no, and it never could have been. VASP registrations were simply national approvals for anti-money laundering rules before the MiCA regulations, not licenses that allowed services to be offered across borders. Even the temporary rules didn’t change this. For example, a company registered in Poland with a six-month grace period couldn’t legally offer services to customers in Austria, where the grace period was twelve months.

Each country’s temporary adjustment period only affected its own territory. Therefore, businesses offering services across borders during this time had to choose one of three methods to operate.

- obtaining a full MiCA CASP authorization,

- ensuring the complete absence of any solicitation directed at users in the target Member State (relying on reverse solicitation),

- or holding multiple domestic VASP licenses across each of the target Member States.

This option would have required the service provider to manage different transition timelines and deadlines in each location, which would have been complex.

July 1st isn’t the key deadline for this transition, as most countries finished their transition periods several months ago.

Myth 2: “Applying Is Just a Matter of Submitting the Paperwork”

In certain areas, the issue isn’t providers being late with their submissions. It’s that there’s no designated place to actually receive the necessary documents.

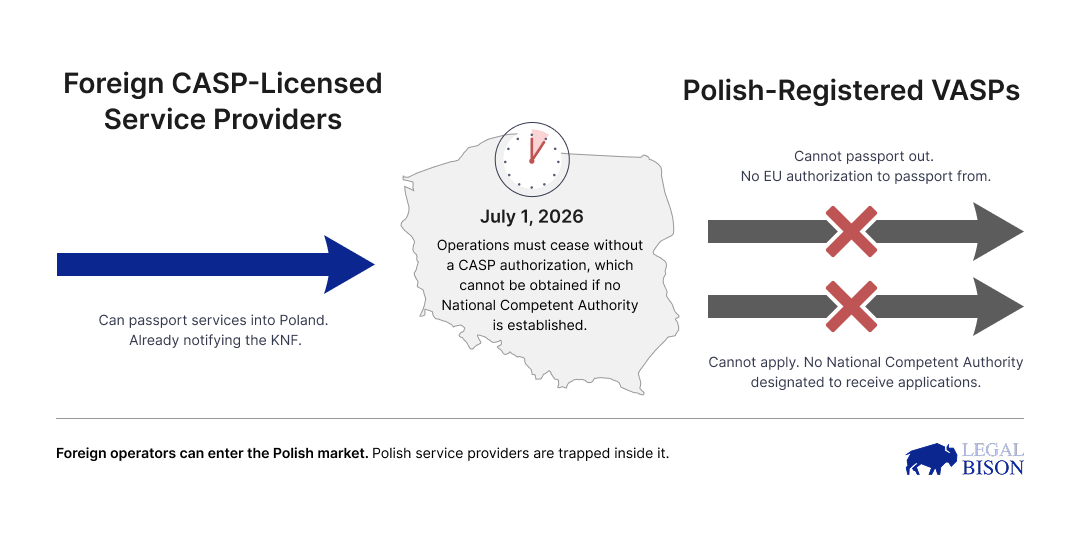

Poland is the clearest illustration. The country’s grandfathering period was set at six months from December 30, 2024, with an implied application deadline around June 2025. That window has passed. But the situation in Poland runs deeper than a missed filing date. In December 2025, the president vetoed the bill that would have enacted the regulation into Polish law, leaving the country without a designated National Competent Authority.

Without a designated government body to handle applications for CASP licenses, service providers couldn’t apply. Poland lacked the necessary regulatory framework, forcing legitimate companies to establish operations in other countries to continue operating legally.

Poland’s financial regulator, the KNF, has clearly stated that registered crypto businesses (VASPs) can operate until July 1, 2026. However, if a dedicated government authority isn’t set up by that date, these businesses will have to stop offering crypto services on July 2nd. The KNF has emphasized that this deadline is firm and cannot be changed by them or through national legislation.

It is a hard stop embedded in EU regulation, not a domestic policy choice.

This situation creates an uneven playing field. Companies from other EU countries with the proper licenses can easily offer their services in Poland by simply informing the Polish financial regulator (KNF). However, Polish companies can’t offer services elsewhere in the EU. They can’t even apply for licenses within Poland, limiting them to the Polish market and facing potential future restrictions. Romania faces a similar problem, with delays in adopting the necessary laws and a lack of clear implementation, as we’ve discussed previously.

How to assess whether a crypto platform is in the gap zone

The following conditions, applied to any crypto platform currently operating in the EU, indicate whether it is relying on grandfathering protection that has already lapsed or is about to:

- Is the platform registered in a Member State that has not enacted its MiCA implementing legislation?

- Did the platform miss its Member State’s CASP application deadline?

- Is the platform currently operating without a pending authorization application filed with a Competent Authority?

The platform is at risk of becoming illegal. Any protections it previously had under older rules will expire on July 1st. This affects all crypto businesses – including exchanges and wallet providers – that people are currently using.

Myth 3: The Reverse Solicitation Escape

A strategy gaining traction among European startup founders involves moving operations outside of the EU, halting marketing efforts directed at EU users, and instead focusing on attracting customers who reach out directly. This allows them to potentially operate without needing an EU license by claiming an exemption for unsolicited business.

As a crypto investor, I’ve been looking into the rules around dealing with firms outside the EU. It’s important to understand that the ‘reverse solicitation’ rule isn’t a loophole for companies who haven’t gotten properly authorized. Basically, it only applies if *I*, as an EU-based client, reach out to a non-EU firm completely on my own – meaning they didn’t contact me or anyone on my behalf first. It’s a very specific situation, and they can’t actively seek me out.

One of the biggest challenges with this test is that ‘solicitation’ isn’t based on having a physical presence. A company doesn’t need an office or legal registration within the EU to be considered as having solicited customers there. ESMA’s report on reverse solicitation guidelines – developed under Article 61(3) – details the various factors that regulators and ESMA itself use to determine if true reverse solicitation is happening.

According to guidelines from ESMA, illegal marketing can happen if anyone closely connected to a firm outside the EU is involved. Regulators will specifically look at the firm’s owners, major shareholders, and leaders to see if they have ties to the EU.

ESMA also specifically points out that offering a website in an EU language not commonly used in international finance suggests an attempt to attract customers. For instance, having a website in Hungarian, Czech, Slovak, or Lithuanian indicates the company is intentionally focusing on residents of a particular EU country, not trying to reach a worldwide audience.

As a crypto investor, I’ve been trying to understand the rules around promoting crypto services in the EU. Basically, any way a company tries to get their services in front of people in the EU – whether it’s through direct ads, partnerships, or even just being listed on a platform – counts as promotion. Having a legal entity *in* the EU isn’t the deciding factor, and neither is *not* having one. It’s just one piece of the puzzle. They’re looking at the bigger picture to see if a service is actively being *offered* to EU residents.

If a service provider is trying to determine if it falls under MiCA regulations, it’s important to understand that the exemption isn’t based simply on where the company is registered. Instead, regulators will look at the company’s overall activities and connections. For example, a service provider with EU-based owners, a platform available in multiple EU languages (even those specific to certain regions), and an affiliate network that attracts EU customers won’t be exempt just because it doesn’t have a registered office in the EU.

Regulators focus on what a company actually does, not any internal descriptions. The key question is whether those actions would be seen as attempts to directly market to customers in that country.

If a company still appears in German or French search results, earns money from EU customers through partnerships, uses country-specific web addresses, or attends events aimed at EU audiences, it hasn’t truly stopped marketing to the EU, and therefore doesn’t qualify for an exemption.

The MiCA compliance implications of getting this wrong extend beyond regulatory sanction. Providing crypto-asset services to EU clients without authorization after July 1 constitutes unauthorized provision of financial services. In EU member states such as Poland, provision of financial services without an authorization is subject to criminal liability. Several have criminalized it. Service providers relying on reverse solicitation as their primary post-July strategy should understand precisely what they are relying on.

Several national regulators are now actively investigating companies they suspect of targeting specific countries. The Dutch AFM and German BaFin, in particular, are taking a firm approach. They issue detailed reports explaining why they believe a service provider is violating MiCA regulations and actively seeking customers. This often leads to requests for interviews, which frequently feel more like interrogations.

| Counts as Solicitation | Reverse Solicitation |

| App available in any localized EU App Store | User navigates directly to the URL with no prior contact from the provider |

| Influencer partnerships where the audience includes EU users | User contacts the platform after discovering it independently through no promotional activity |

| Website available in a local EU language or using a country-code domain (.pl, .ro) | User explicitly and independently initiates the service relationship, supported by factual records tracking the interaction |

| Geo-targeted social content or paid digital placements reaching EU users | No localized UX, no marketing materials, and no promotional activity preceded the contact |

The Arithmetic of “Pending”

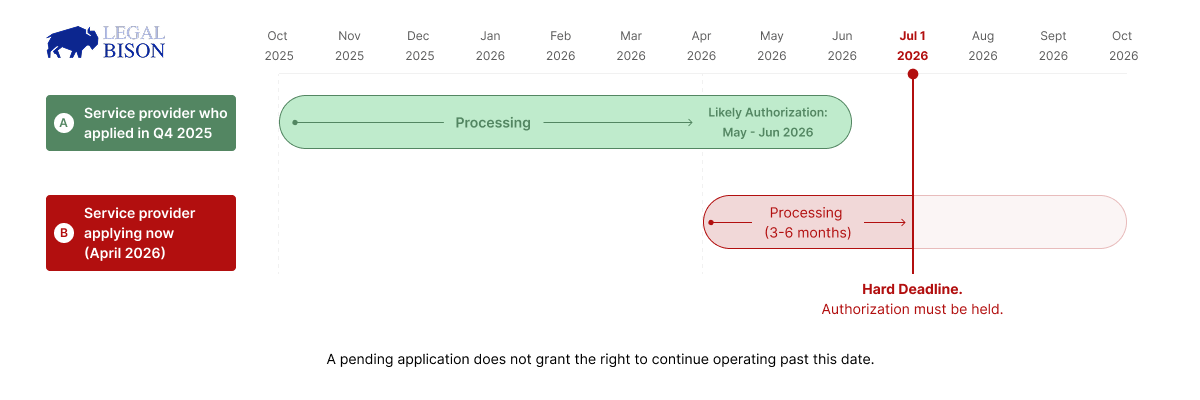

The situation is more complicated, but equally pressing, for service providers who have applied for authorization but haven’t received it yet.

Simply applying for authorization isn’t enough. You must receive official approval before July 1, 2026, or you won’t be allowed to continue operating. The rules require full authorization, not just a submitted application, before the temporary period ends.

- A service provider whose application is complete, submitted in a well-resourced jurisdiction, and moving through the review process may receive the necessary authorization before the deadline.

- A service provider whose application is incomplete, filed recently, or sitting in a jurisdiction with a congested pipeline may not.

Once the deadline has passed, there’s no automatic right to keep operating while a review is happening. If you’re a service provider in this situation, you need to be in direct contact with your National Competent Authority to understand your specific deadlines. Relying on assumptions isn’t a good way to ensure you’re meeting requirements at this point.

Beyond the European Union, Iceland and Liechtenstein, through their connection to the European Economic Area, also set a deadline of around July 2026 for changes. This deadline isn’t just for EU countries, but applies to all members of the European Economic Area.

Restructuring: What It Actually Involves

If service providers face roadblocks in getting authorized in certain areas, they still have one way to keep operating: they can restructure their business and obtain a license from a qualified service provider (CASP) in a region where the authorization process is open and applications are being reviewed.

Several countries within the European Union are now fully set up to handle and approve applications for crypto-asset service providers (CASP). Malta, Austria, Ireland, and Lithuania are leading the way, with their regulatory systems in place and applications currently being processed. It’s important to note that each country has slightly different requirements for what qualifies as an acceptable substance, and these requirements are just as important as how long the approval process takes.

Moving a company’s restructuring process to another country within the EU isn’t just about getting approval. It also requires handling several practical details, such as:

- Establishing the legal entity in the target jurisdiction with genuine governance and operational presence, not a shell registration.

- To satisfy the authorization requirements, the firm must have its share capital paid up in an account with a formal credit institution (notably, an account with an EMI or a Payment Service Provider/PI is not sufficient). While this bank account does not strictly need to be located in the target jurisdiction, establishing this relationship should begin as early as possible, as onboarding crypto businesses is a rigorous process that does not automatically follow from simply filing for a license.

- Ensuring the complete cessation of prior EU activities before relying on a non-EU licensing position. A service provider that relocates its primary licensing to a non-EU jurisdiction, yet maintains an active EU legal entity or continues to service EU users under a legacy VASP registration, has not effectively resolved its regulatory exposure. Under MiCA, providing crypto-asset services within the Union strictly requires an active EU authorization. Third-country firms are broadly prohibited from providing crypto-asset services in the EU and cannot bypass these requirements while maintaining an operational footprint in the bloc.

- Understanding the strict reverse solicitation restrictions that apply to the existing EU client base. According to ESMA’s Final Report on the guidelines on reverse solicitation under MiCA, EU-regulated entities are explicitly prohibited from soliciting or redirecting EU clients to crypto-asset services provided by a third-country firm, even if that firm is part of the exact same corporate group. A non-EU licensed service provider cannot solicit its former or prospective EU users into its new non-EU structure. This prohibition encompasses any person or entity acting on the third-country firm’s behalf, this means that commercial arrangements functioning as user acquisition channels, even if framed as B2B partnerships, affiliates displaying backlinks, or influencers, are considered unlawful solicitation. As a consequence, transitioning an existing user base across a jurisdictional restructuring requires meticulous handling, as simply redirecting users to the non-EU entity’s website or app constitutes a breach of the reverse solicitation rules.

If service providers don’t receive approval by July 1st, they’ll need to temporarily stop providing services. They can still work on their applications during this pause, and once approved, they can resume operations.

Banks are now contacting customers who are only registered as VASPs to let them know that banking services will be discontinued after July 1st if they can’t prove they’ve applied for or obtained a CASP license.

From my analysis, while business disruption is a definite possibility, it’s usually temporary. Specifically, for service providers who’ve proactively submitted a solid application to the relevant authority and have a working relationship with them, the period of interruption could be quite limited.

The biggest problem is for service providers who haven’t started the filing process yet. They’re trying to quickly complete what usually takes months, and they have very little time left before the deadline.

What This Article Decoded

There’s been a lot of misunderstanding about how MiCA handles existing crypto assets. Here’s a clear explanation of what the regulation actually says:

The July 1, 2026 date isn’t when service providers needed to take action—it’s the deadline for having authorization in place. For most countries in the EU, the important application deadline was actually between June and December 2025. Service providers who missed their country’s deadline won’t be able to rely on existing protections.

Before the MiCA regulation, simply registering as a VASP (Virtual Asset Service Provider) in one EU country didn’t automatically allow a company to offer services in other EU countries. This registration was a national anti-money laundering designation, not a license that could be used across borders. The temporary rules put in place after the initial regulations actually strengthened this restriction, rather than removing it.

Regarding the lack of laws in some areas: If a country hasn’t passed the necessary laws, it doesn’t have an official body to accept applications for certification. This creates a serious issue for service providers in those countries – it’s more than just missing a deadline. They can’t apply for certification locally, they can’t transfer it from another country, and they’ll be forced to stop operating on July 1st, even if they plan to comply with the rules. This means they’ll have to temporarily halt services or get approval from a different country.

Regarding reverse solicitation: This exemption isn’t something companies can use *after* they’ve already started operating in the EU. It only applies to firms based outside the EU that aren’t actively trying to do business with people in the EU. A service provider already registered in the EU can’t use it. Even if a non-EU firm has stopped doing business in the EU, they need to make sure any remaining activities don’t count as actively seeking EU customers. According to ESMA, things like appearing in online searches (SEO), working with affiliates or influencers, and even promoting services at conferences could be considered illegal attempts to reach EU users.

Looking ahead, getting the necessary approvals takes a long time. Applications submitted now won’t guarantee continued service beyond July 1st. Providers who haven’t applied yet are unlikely to have a solution in the next three months. The key question is whether it’s even possible to fully establish operations and meet all requirements within the limited time remaining. We’ll examine the typical length of the CASP application process next week.

This article was produced in partnership with LegalBison. The content is for informational purposes only and does not constitute legal advice.

Read More

- Gold Rate Forecast

- BTC PREDICTION. BTC cryptocurrency

- NEAR PREDICTION. NEAR cryptocurrency

- USD CNY PREDICTION

- Brent Oil Forecast

- EUR CNY PREDICTION

- TON PREDICTION. TON cryptocurrency

- USD JPY PREDICTION

- WLD PREDICTION. WLD cryptocurrency

- UB/USD

2026-04-04 13:00