The Death Cross of Ether: A Ballet of Bankruptcy or a Bear Market Masquerade?

//media.crypto.news/2026/02/ETHUSDT_2026-02-18_13-03-19.webp”/>

//media.crypto.news/2026/02/ETHUSDT_2026-02-18_13-03-19.webp”/>

Since its halcyon days of support, our beloved cryptocurrency has floundered in its quest for renewed vigor, much like a fish out of water gasping for the sweet embrace of liquidity. Analysts, those modern-day oracles, caution us that a cocktail of macroeconomic jitters and lackluster buying enthusiasm may very well plunge this digital darling back towards the murky depths of the $50,000 abyss-a realm not frequented since the sun-drenched September of 2024.

Ah, but dear reader, the plot thickens! This deal not only consolidates businesses tied to the ever-magnanimous Bailey-who co-founded BTC Inc. and later launched UTXO Management-but also brings these enterprises under one roof, like a family reunion where everyone awkwardly avoids discussing politics.

In a most fortunate turn of affairs, Stripe’s stablecoin division, known as Bridge, has received conditional approval from the illustrious Office of the Comptroller of the Currency (OCC) to launch a federally chartered national trust bank. This development permits Bridge to operate with that reassuring governmental oversight which one so desires.

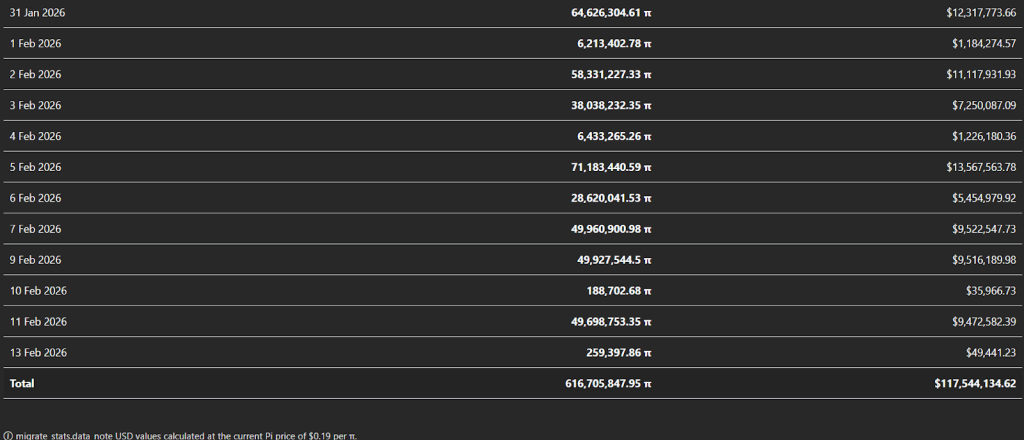

With sentiments stabilizing across this raucous market, PI’s unexpected vigor is certainly catching the eye, particularly as structural supply pressure appears to be taking a breather. One cannot help but wonder: is this the giddy excitement of pre-anniversary jubilation, or merely the first signs of a broader breakout? The suspense is positively thrilling!

In a move that can only be described as either brave or downright foolish, these firms went ahead and nabbed themselves some shares in the iShares Bitcoin Trust, a spot Bitcoin ETF managed by none other than the financial giant BlackRock. This just goes to show that folks will still chase after regulated crypto investments like moths to a flame, despite the market behaving more like a rollercoaster than a stable vehicle.

Gemini just threw a corporate party so chaotic, even a toddler could see the chaos. Three senior execs are bailing, and the company’s trying to act like this isn’t the equivalent of a reality TV finale. Meanwhile, they’re ditching markets faster than a broke friend at a buffet. Spoiler: It’s not a happy ending.

Ah, Polygon, that modest yet ambitious contender, has achieved a victory both subtle and profound, overtaking Ethereum in the daily toll of fees. Recent chronicles reveal Polygon’s coffers swelling past the $300K mark, a testament to its growing allure in the labyrinthine world of blockchain. How quaint, that such a triumph should stir the hearts of the technologically besotted!

Now, if you’re wondering why this sudden exodus is happening, let’s just say it’s not because they suddenly remembered they left the oven on. According to a report from CryptoQuant (which sounds like a superhero for crypto enthusiasts), the miners aren’t playing favorites either. They’ve snatched up about 12,000 BTC from Binance, while the other 24,000 BTC got scattered across various exchanges like confetti at a New Year’s party. Clearly, this isn’t a case of a few miners deciding to throw a farewell party at one casino.

Eagle Crypto, that modern-day Raskolnikov of the crypto world, has unearthed a silent reward payout tied to the historical use of Chainlink. A reward, you say? How quaint. Yet, this revelation coincides with a heightened sensitivity in LINK’s price-a sensitivity so acute, one might mistake it for the tormented conscience of a man burdened by his own greed. When the commentary was made, LINK stood above its short-term support, a fleeting moment of pride before the inevitable consolidation, a metaphor for the human soul’s struggle against its own insignificance.