Ah, dear MicroStrategy, once a gallant knight in the shimmering armor of cryptocurrency, now finds itself besieged by an army of market woes as Bitcoin tumbles to the modest height of $60,000! The company’s crypto treasury, a veritable treasure chest, lies buried beneath its average acquisition cost like a forgotten relic of a bygone era, stirring fresh anxiety about its balance-sheet integrity.

As Bitcoin takes a nosedive, shares of this beleaguered enterprise plummet with a grace reminiscent of a melodrama. It appears that MicroStrategy has become the leveraged proxy for Bitcoin’s misadventures, with its stock value now teetering below the actual worth of its precious Bitcoin holdings. This signals a rather alarming stress test for their treasury model-one that would make even the sturdiest of hearts quail.

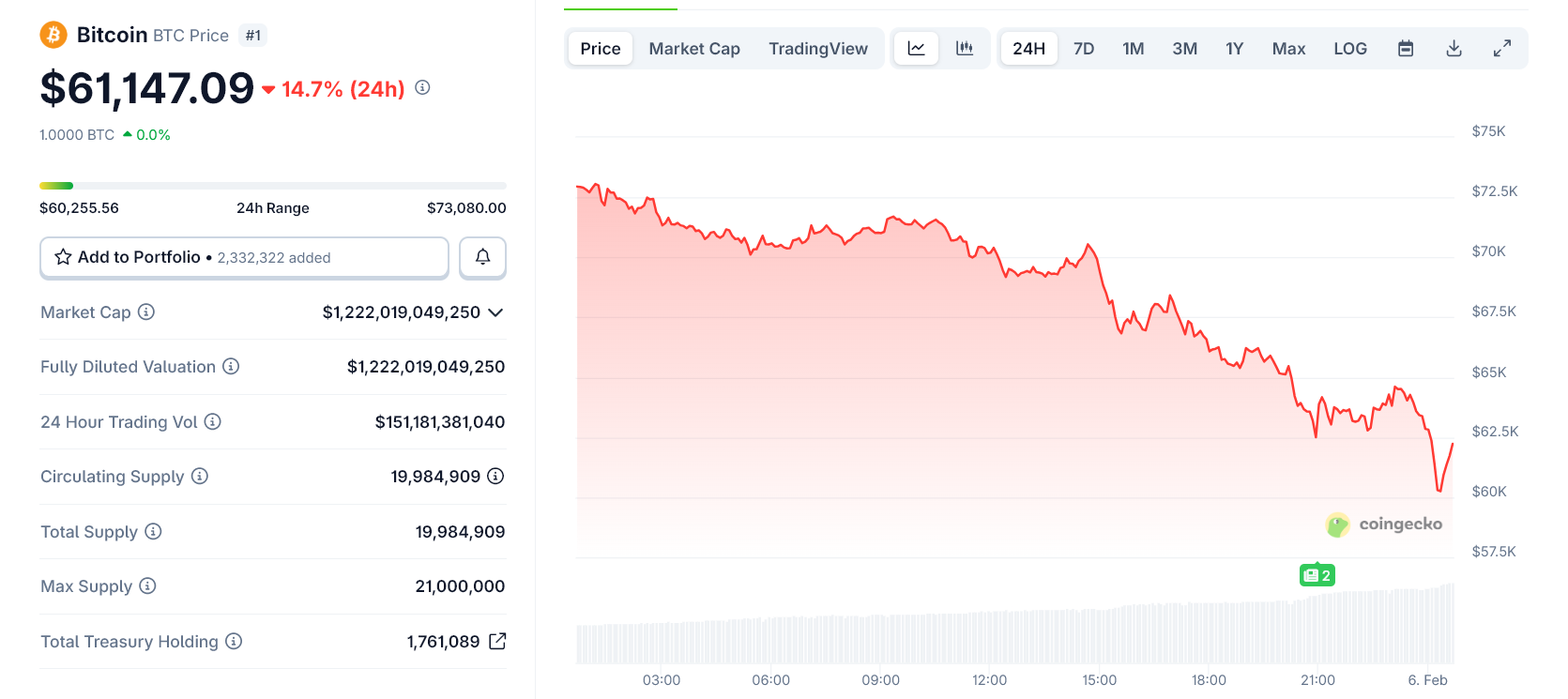

Bitcoin Price Crashes to a Yearly Low of $60,000

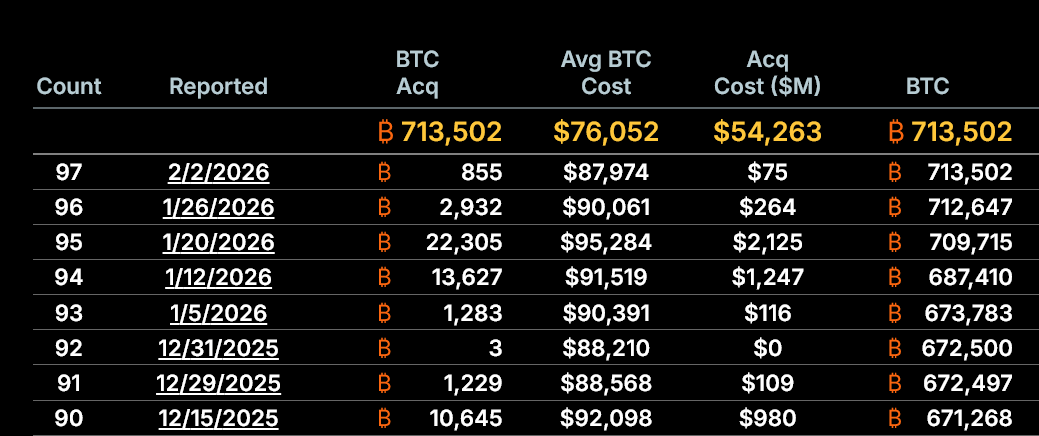

MicroStrategy, bless its soul, clutches approximately 713,500 Bitcoin, procured at the extravagant price of about $76,000 per coin. Now, with Bitcoin flirting with the tantalizing figure of $60,000, the company’s holdings languish roughly 21% below cost basis, manifesting as billions in unrealized losses-because who doesn’t enjoy a good tragedy?

These losses, though unrealized and not demanding immediate asset liquidation, do cast a shadow over MicroStrategy’s equity narrative, transforming it from a tale of triumph to one of woe. Investors, caught in this dramatic shift, may find themselves pondering the virtues of short-term survival over the allure of long-term accumulation.

Market Premium Collapses Below Asset Value

But wait! The plot thickens! For our intrepid MicroStrategy, a more pressing dilemma arises: its market net asset value (mNAV) has descended to a dismal 0.87x. In layman’s terms, the stock now trades at a discount to the value of the Bitcoin on its balance sheet-a situation that could make even the most optimistic souls weep.

This discount is no mere trifle, for MicroStrategy’s grand strategy hinges on issuing equity at a premium to fund further Bitcoin escapades. With the premium evaporated like mist in the morning sun, any new shares would be more dilutive than a bad gin and tonic, effectively freezing the company’s growth ambitions.

Strategy and Michael Saylor Still Have Some Short-Term Protection

Yet, fear not, dear readers! The apocalypse has not yet arrived; MicroStrategy is not quite on the precipice of insolvency. The firm has previously raised a staggering $18.6 billion through equity issuance over the last two years, mostly during balmy market conditions. These capital raises have allowed the company to amass its Bitcoin horde without excessive dilution-an achievement worthy of a round of applause.

Moreover, with debt maturities stretching into the horizon, and no margin-call mechanisms linked directly to Bitcoin’s spot price at present levels, it seems there remains a flicker of hope amidst the chaos.

The Real Risk Lies Ahead

Ah, but heed well! MicroStrategy has transitioned from an ambitious expansion phase into a defensive crouch. Catastrophic risk looms larger if Bitcoin lingers below its cost for an eternity, if mNAV remains shackled, and if capital markets continue to play coy.

In such a dismal scenario, refinancing could turn into a Herculean task, dilution risks would swell like the tide, and investor confidence might erode faster than a sandcastle before the rising waves.

For the moment, MicroStrategy remains afloat, though the margins for error have thinned drastically, leaving the company precariously poised for the next chapter in Bitcoin’s tumultuous saga.

Read More

- BTC PREDICTION. BTC cryptocurrency

- Bitcoin’s Wild Ride: Whales Strike Back, Shorts Cry 😭💰

- Shocking Rally Ahead for NIGHT Token: Analyst Predicts 4x Surge to $0.20!

- Bitcoin’s Cosmic Cringe: Why the Crypto World Is Now a Black Hole 🌌💸

- SEC’s Peirce Champions Crypto Privacy as Tornado Cash Trial Heats Up 🚒💼

- 🚀 NEAR Protocol Soars 8.2% While Others Stumble – CoinDesk 20 Chaos! 💸

- ETH PREDICTION. ETH cryptocurrency

- Ethena’s $106M Token Unlock: Will Aave’s Liquidity Bust or Just a Bad Hair Day? 🤔

- Litecoin’s Wild Ride: $131 or Bust? 🚀💰

- Binance Now Fully Approved in Abu Dhabi-What This Means for Crypto!

2026-02-06 04:37