What to know:

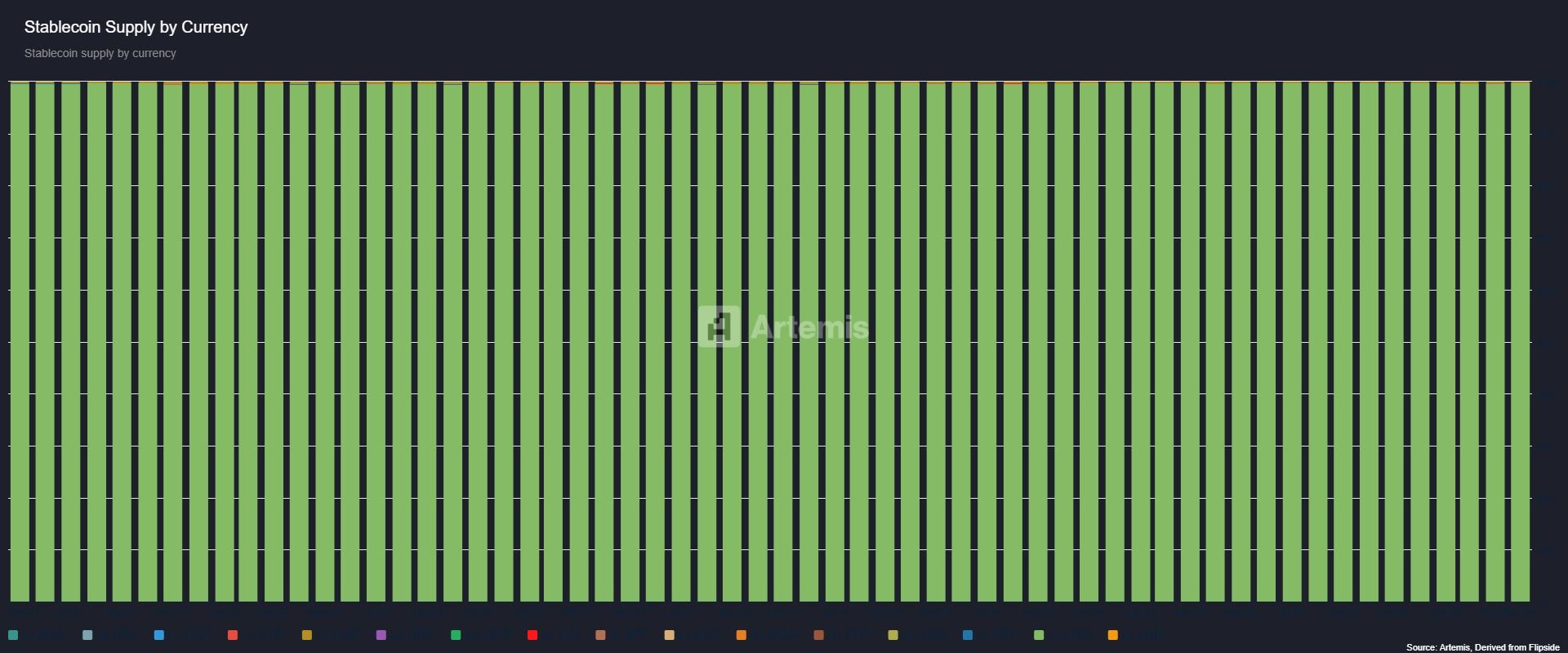

- Non-dollar stablecoins have grown in supply to about $771 million since 2021, but their share of the stablecoin market has edged down to just 0.24%.

- Dollar-pegged stablecoins benefit from access to deep, liquid U.S. Treasury markets, with about $15.4 billion in tokenized U.S. government debt far outstripping non-U.S. tokenized government bonds.

- Because most national currencies lack meaningful international liquidity, only a handful can plausibly support global stablecoins, leaving dollar-based tokens overwhelmingly dominant.

Stablecoins that aren’t backed by the U.S. dollar have increased in popularity over the last five years, but they haven’t actually gained any significant ground in the overall market. Despite all the recent attention, their importance remains limited.

According to data from Artemis, the total supply of stablecoins not pegged to the US dollar – including the euro, Canadian dollar, Japanese yen, and Singapore dollar – grew from $261 million in May 2021 to around $771 million in April 2026. However, despite this increase, these non-USD stablecoins now represent only 0.24% of the overall stablecoin market, leaving dollar-pegged tokens dominating with 99.76%.

The U.S. dollar’s leading position in global finance is gradually weakening. While it still handles 89% of foreign exchange transactions, accounts for 61% of international debt, and makes up 57% of global reserves, these figures have been steadily declining over the past ten years.

Onchain, it’s the opposite.

Increasing Treasury yields could strengthen the benefits of dollar stablecoins. These stablecoins aren’t only supported by the world’s main currency, but also by a growing amount of short-term U.S. government debt.

When investment returns increase, companies that issue short-term government debt can boost their earnings. This makes it more profitable to create dollar-backed stablecoins, allowing major firms to invest more in growing their reach through things like marketing, distribution networks, and strategic alliances.

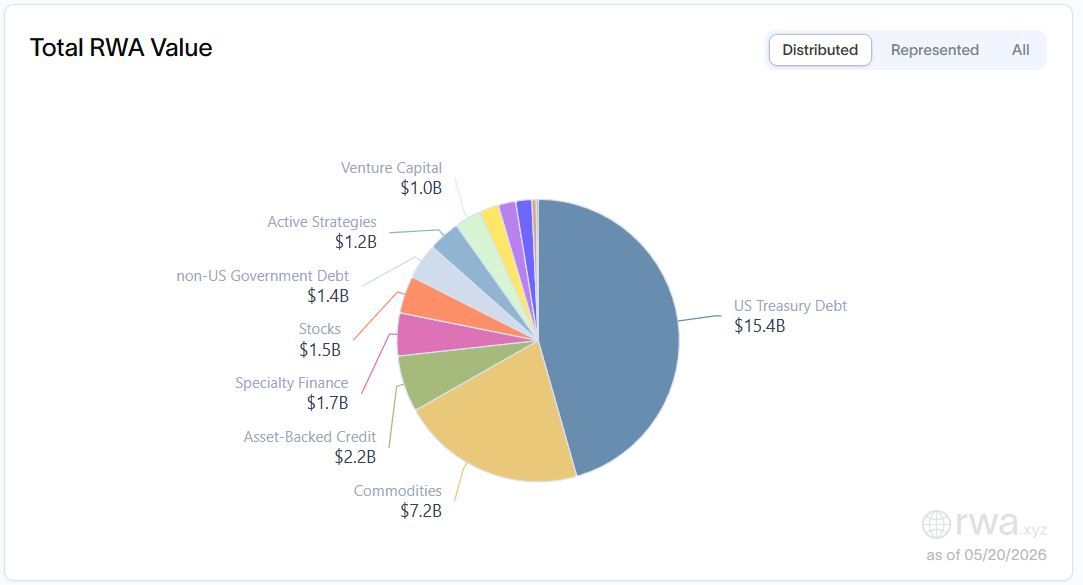

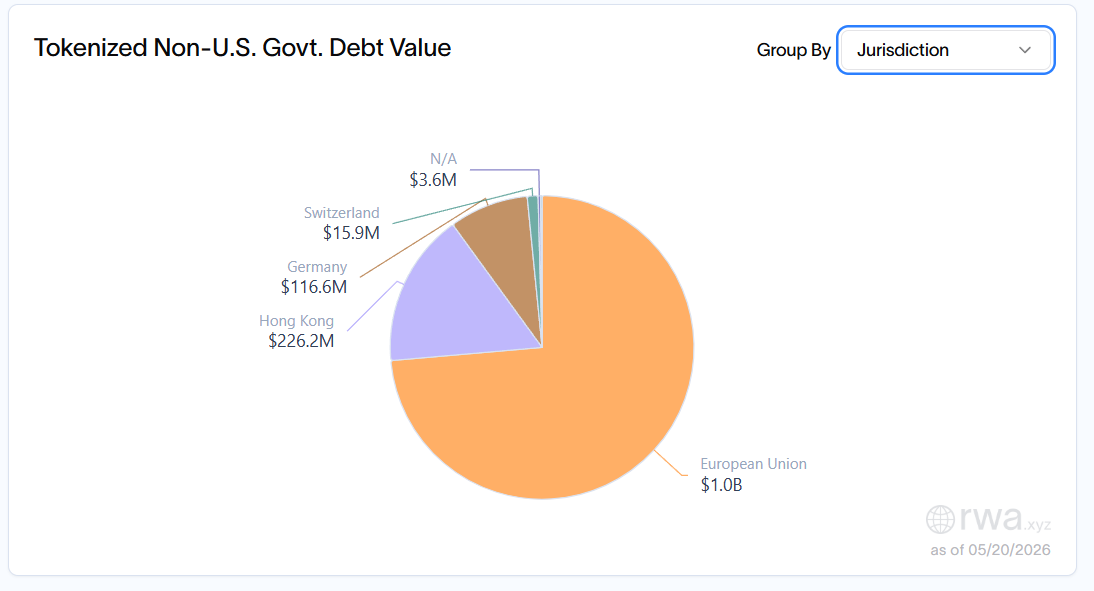

We’re already seeing the benefits of U.S. Treasury bonds being available on the blockchain. Currently, $15.4 billion worth of tokenized U.S. Treasury debt exists, making it the most popular type of real-world asset (RWA) tracked by RWA.xyz. This is significantly larger than the market for tokenized bonds from other countries, which totals only $1.4 billion – meaning the U.S. Treasury market on the blockchain is about 11 times bigger than all other government bond markets combined.

This is important for stablecoins because those backed by the US dollar have access to a large, easily accessible pool of assets that also earn returns. Stablecoins based on other currencies, however, are trying to establish markets without a similar foundation of reserves.

As an analyst, I’ve been looking into why dollar-backed stablecoins continue to dominate the market, and a key factor is reserves. To reliably handle redemptions – when people want to exchange their stablecoins for actual dollars – issuers need highly liquid and trustworthy assets as backing. Currently, the most readily available and trusted option for this, especially on the blockchain, is short-term U.S. government debt.

At the recent CoinDesk Consensus conference in Hong Kong, John Turner, Coinbase’s head of stablecoins, explained that Coinbase’s leading position in the stablecoin market quickly became stronger because of its high liquidity. He noted that having ample liquidity attracted trading volume, which in turn further increased liquidity.

More liquidity led to increased trading activity, which in turn encouraged the development of practical applications, and those applications drew in even more liquidity. This creates a positive cycle that currencies other than the dollar haven’t been able to achieve.

The reason for this difference is straightforward: most traditional currencies aren’t accepted in countries other than the one they’re issued in.

The International Monetary Fund monitors around 180 currencies used around the world. However, only about eight of these are actively and widely traded in global foreign exchange markets: the U.S. dollar, euro, Japanese yen, British pound, Swiss franc, Canadian dollar, Australian dollar, and Chinese yuan. Most other currencies are primarily used within their own countries. For example, currencies like the Taiwan dollar and the Korean won have restrictions that limit their use outside of their home countries.

Stablecoins benefit from the global acceptance of the currency they’re based on, something most currencies around the world don’t have.

This means only a few major currencies – perhaps around six, such as the euro or the yen – are strong enough to reliably back a stablecoin used worldwide.

But the market doesn’t seem interested for now.

Read More

- USD RUB PREDICTION

- APT PREDICTION. APT cryptocurrency

- ZEC PREDICTION. ZEC cryptocurrency

- USD JPY PREDICTION

- PEPE PREDICTION. PEPE cryptocurrency

- WLFI PREDICTION. WLFI cryptocurrency

- HYPE PREDICTION. HYPE cryptocurrency

- SOL PREDICTION. SOL cryptocurrency

- Gold Rate Forecast

- USD CNY PREDICTION

2026-05-20 09:16