In the grand theater of corporate finance, few vows have been so solemnly sworn as Mr. Michael Saylor’s resolute pledge to “never sell” one solitary Bitcoin. For nigh on five years, Strategy Inc.-formerly MicroStrategy, now the undisputed sovereign of on-balance-sheet BTC holdings-has built its empire upon this simple creed: buy, hold, and let the asset appreciate. Alas, on the fateful 5th of May, 2026, this sacred pact cracked like a brittle teacup dropped by a clumsy parlormaid.

During the quarterly earnings call, Mr. Saylor, Strategy’s esteemed founder and executive chairman, uttered words that sent tremors through the crypto markets and traditional finance alike: “We will probably sell some Bitcoin to pay a dividend just to inoculate the market and send the message that we did it.” A bold declaration, indeed, as if one might quell gossip by whispering it oneself.

Mr. Saylor, ever the strategist, framed the move not as a capitulation but as a masterstroke of engineering: “You buy Bitcoin with credit, you let it appreciate, and then you sell Bitcoin to pay the dividend.” A logic as sound as a well-ventilated drawing room, though one might question whether such a maneuver truly constitutes “engineering” or merely a desperate bid to silence the murmurs of short-sellers.

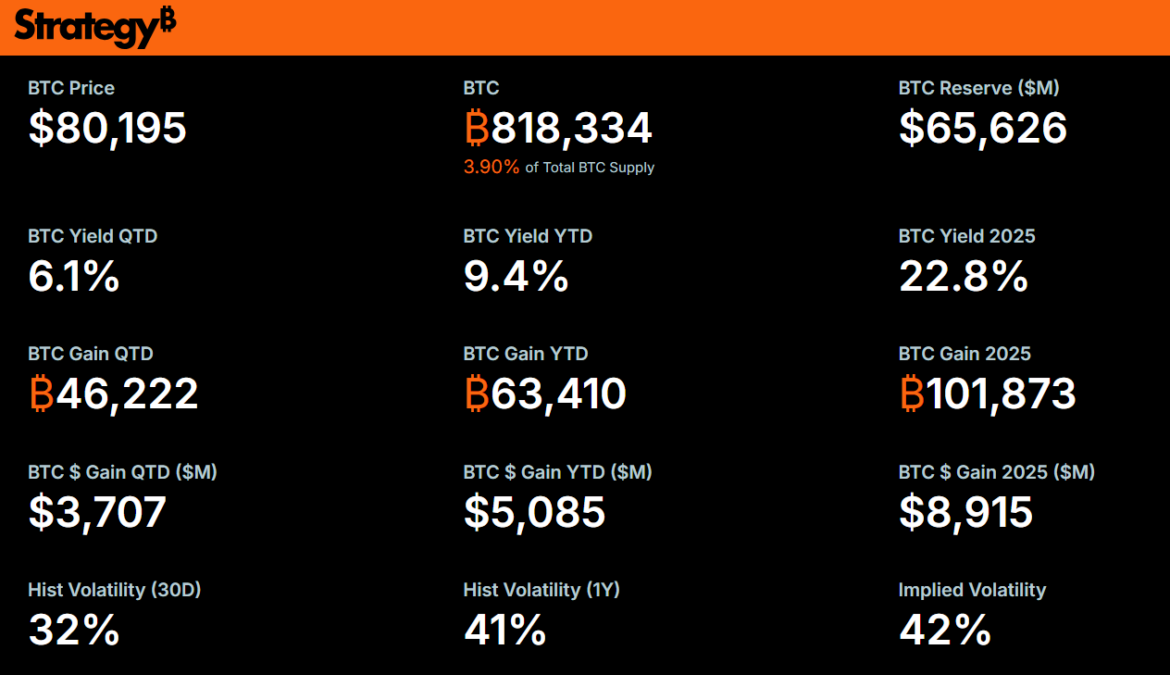

The timing, as fate would have it, was anything but coincidental. Strategy had just endured a net loss of $12.54 billion in Q1, a sum so staggering it might make even a Rothschild wince. Yet the company’s Bitcoin hoard-818,334 BTC, or roughly 3.9% of all Bitcoin ever to exist-remained a fortress of wealth, acquired at a blended cost of $75,537 per coin. A fortune, to be sure, though one might argue that holding such a treasure in a digital vault is akin to keeping a cask of claret in a room prone to damp.

The Demise of the Pure HODL Era?

Strategy’s Bitcoin odyssey began in 2020 as a daring hedge against fiat currency’s inevitable debasement. What began as opportunistic purchases soon swelled into a full-blown treasury strategy, transforming a modest business-intelligence firm into a leveraged Bitcoin proxy. By late 2025, the company had rebranded to Strategy, a name as grand as a duke’s estate, for Bitcoin had ceased to be a side bet and become the main event.

Central to this new order was the 2025 launch of STRC-“Stretch”-a perpetual preferred stock as audacious as a debutante’s gown. Backed by the Bitcoin balance sheet, STRC pays a variable cash dividend, currently fixed at 11.5% annualized. It has scaled to $8.5 billion in notional value, a feat that might make even a Rothschild blush. Yet such success bred obligations, for the company’s annual dividend and interest payments now run about $1.5 billion. A sum, one might suppose, that could fund a rather lavish ball, though perhaps not a lifetime of dividends.

The growing dividend load created a structural tension: how to raise capital, service credit-like instruments, and avoid diluting common shares without touching the crown jewel? A conundrum as thorny as a rose garden in spring, though one suspects Mr. Saylor’s solution involves more calculus than roses.

A New Playbook: Net Aggregator, Not Passive Holder

Mr. Saylor and CEO Phong Le spent much of the earnings call outlining a more active balance-sheet philosophy. The goal, they insisted, remains “net aggregation” of Bitcoin-growing the total stack while, more importantly, increasing Bitcoin per share (BPS), a metric as precious to equity investors as a well-tied cravat to a dandy.

Tune into @Strategy’s Q1 Earnings Call live now on X. We’ll cover:

-Q1 financial results

-Digital Credit $STRC

-Digital Equity $MSTRFollowed by a live Q&A!

– Strategy (@Strategy) May 5, 2026

Sales, if they occur, would be surgical: likely higher-cost-basis coins to harvest tax losses or fund obligations in a way that proves accretive rather than dilutive. A strategy as precise as a surgeon’s blade, though one might question whether such precision can truly offset the moral hazard of betraying a “never sell” vow.

Mr. Le, ever the pragmatist, declared, “We’re not going to sit back and just say, ‘We’ll never sell the bitcoin.’ We want to be net aggregators of bitcoin-increasing our total bitcoin, but more importantly, increasing our bitcoin per share.” Mr. Saylor likened the company to a real-estate developer who occasionally sells a parcel to unlock value elsewhere. A metaphor as charming as it is disingenuous, for few would accuse a developer of “unlocking value” when selling a plot to fund a new purchase.

In one illustrative scenario, the firm could hold a modest USD reserve and service all obligations purely through modest Bitcoin sales-driving an even higher BTC yield for shareholders without tapping equity markets at all. A plan as elegant as a well-ordered estate, though one might argue that such a strategy relies on the same alchemy as turning lead into gold.

The “inoculation” comment was classic Saylor theater-acknowledging that the mere idea of a sale would rattle purists and short sellers, so why not get the first small transaction on the record and demonstrate that the sky does not fall? A tactic as theatrical as a stage magician’s flourish, though one suspects the true test lies not in the performance but in the aftermath.

A hypothetical $100 million Bitcoin sale, he noted, would represent a negligible fraction of the treasury and might even be net positive for the broader Bitcoin network by adding liquidity and proving institutional flexibility. A sentiment as optimistic as a gambler’s last throw of the dice, though one might question whether such a sale would truly “prove” anything beyond the company’s willingness to bend its own rules.

Market Reaction: Jitters, the Reflection

Following the announcement, Strategy shares (MSTR) dropped more than 4% in after-hours trading on May 5, while Bitcoin briefly dipped below $81,000. The move fueled a brief wave of commentary: some hailed it as pragmatic maturity; others saw it as the first crack in the armor that had made Strategy the poster child for corporate Bitcoin adoption. A schism as dramatic as a duel in a drawing room, though one suspects the real drama lies not in the opinions but in the numbers.

However, the shift does not alter the core thesis-Strategy remains overwhelmingly long Bitcoin and continues to outpace spot ETFs in net accumulation via its capital-structure alchemy. Yet it reframes the company less as a pure “Bitcoin ETF with software attached” and more as a dynamic Bitcoin development firm that can flex between issuance, appreciation, and selective realization. A transformation as subtle as a lady’s change of gown, though one might argue that such a shift is more akin to a metamorphosis than a mere alteration.

Short sellers who bet on inevitable dilution to fund dividends now face a counter-narrative: the firm can service its credit without flooding the market with new MSTR shares. A revelation as startling as discovering a rival’s secret ploy, though one suspects the true test lies in the execution, not the theory.

At the time of publishing, MSTR was priced at $179.84, giving the company a market cap of $63.114 billion. While BTC was trading near $80,255-putting Strategy’s Bitcoin reserve valued at $65.67 billion. Figures as impressive as a well-counted fortune, though one might question whether such numbers truly reflect the company’s long-term viability or merely its current whims.

What It Means for the Corporate Bitcoin Playbook

The announcement arrives at a pivotal moment as Strategy’s success has inspired dozens of smaller firms and even pushed some sovereign entities to explore Bitcoin reserves. Its pivot signals that even the most committed treasury strategy must eventually confront real-world cash-flow mechanics once preferred obligations scale into the billions. A truth as inescapable as the passage of time, though one suspects the true challenge lies in maintaining conviction while adapting to circumstance.

The math still favors the bulls: at current BTC appreciation rates, the treasury grows faster than the dividend drain. But the rhetorical bridge from “never sell” to “strategic offloading” forces every Bitcoin treasury manager to ask the same question: when does disciplined management become compromise? A quandary as thorny as a rose garden in spring, though one suspects the answer lies not in the question itself but in the courage to act.

Mr. Saylor himself has not wavered on the long-term conviction. As shown on the company’s official website, its KPIs-BTC Yield (9.4% year-to-date), BTC Gain (63,410 coins added), and BPS growth-remain the scoreboard. Metrics as precise as a well-timed dance step, though one might argue that such precision offers little solace when the dance floor is treacherous.

No sales have been executed as of this writing, and the press release itself stayed silent on the topic, focusing instead on capital raised ($11.68 billion year-to-date) and the proposal to shift STRC dividends to semi-monthly payments for better liquidity and price stability. A silence as telling as a lady’s averted gaze, though one suspects the true story lies not in what is said but in what is omitted.

Yet the message is unmistakable. Strategy is no longer content to be a static vault. It wants to be an active steward-buying aggressively when markets allow, engineering yield-bearing instruments like STRC, and, when accretive, trimming the smallest slice necessary to keep the machine humming. In Mr. Saylor’s words, it creates “more optionality and second- and third-order effects” for equity holders. A vision as grand as it is vague, though one might question whether such “optionality” is truly an advantage or merely a distraction.

This evolution’s impact on Strategy’s Bitcoin-maximalist roots will face its first real tests in the coming months. The shareholder vote on dividend frequency looms as an early indicator, followed closely by any announcement of the company’s inaugural modest sale. Trials as fraught as a courtship, though one suspects the true measure of success lies not in the outcome but in the resilience of the company’s convictions.

For now, the world’s largest corporate Bitcoin holder has signaled it is ready to evolve. The era of absolute HODL is over. The age of calculated, dividend-aware offloading has begun. A transition as inevitable as the changing of the seasons, though one might argue that the true test lies not in the transition itself but in the ability to navigate it without losing sight of the original purpose.

Read More

- Bitcoin at Halfway Through Halving: Gains Lag Behind Previous Cycles

- Unlock Exclusive Access to OpenGradient’s AI Token Launch on Binance and PancakeSwap!

- Silver Rate Forecast

- USD CLP PREDICTION

- XRP Holders Beware: EarnXRP’s Hidden Fees and Risks Exposed by Analyst

- Solana Developers Panic Over Quantum Threats (But You Won’t!)

- JPY KRW PREDICTION

- WLD PREDICTION. WLD cryptocurrency

- USD CNY PREDICTION

- BNB CAD PREDICTION. BNB cryptocurrency

2026-05-08 14:49